The end of each year provides an opportunity to look back, reflect, and contemplate the year ahead. When reflecting on 2022, it’s clear it was a big year of transformation in many ways.

From an economic perspective, three major trends impacted banks and credit unions and caused a dramatic shift in their balance sheets. These 2022 banking trends include:

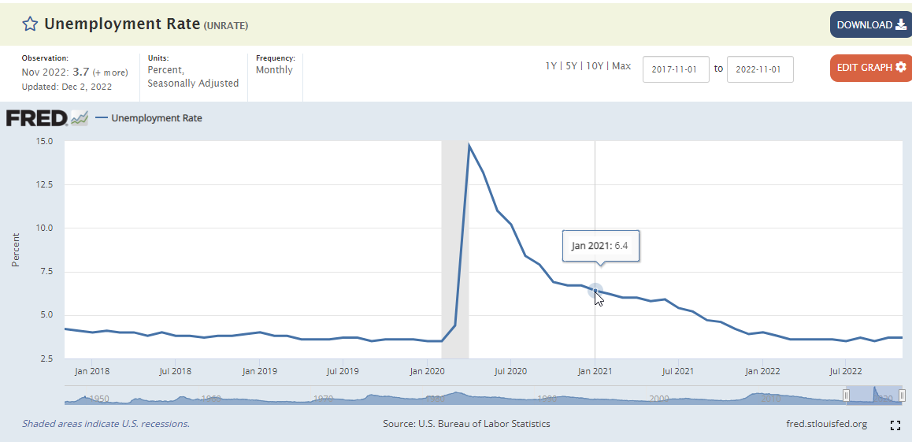

- Unemployment – The combination of very low unemployment rates and historically low labor force participation has made it extremely difficult to hire and retain employees, which has also driven wage increases. (See unemployment and labor force participation charts below.)

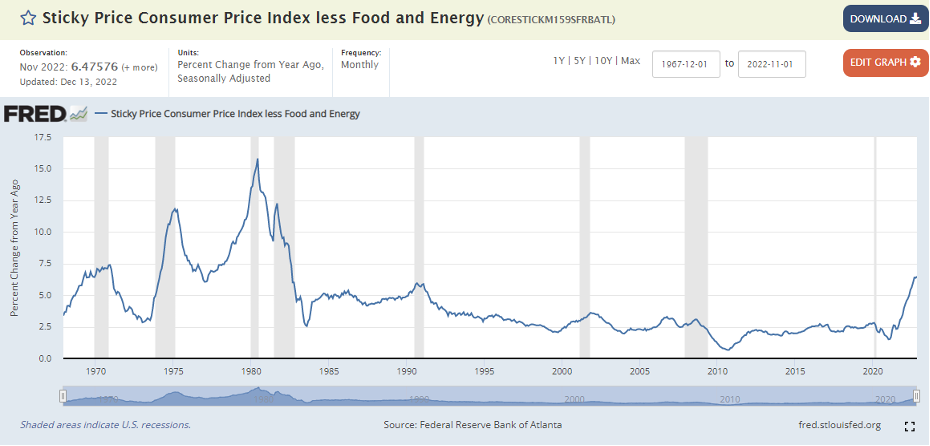

- Inflation – Inflation has risen dramatically over the past year and the “sticky price consumer price index less food and energy” hit 6.47% in November 2022 – a level not seen since the early 1980s! (See Sticky Price Consumer Price Index less Food and Energy below.)

- Interest Rates – Given the high level of inflation, the federal reserve has made dramatic increases in the fed funds rate of over 4.00% – resulting in increased borrowing costs for all products. Additionally, the 30-year mortgage rate hit above 7.00%.

Each of these macro-economic factors have impacted financial institutions and how you reposition your balance sheets in significant ways.

The FDIC’s quarterly publication of industry-wide financial data indicates some dramatic shifts in bank balance sheets from January 1, 2022, to September 30, 2022, including:

- Deposits shrinking by 1.75%.

- Investment portfolios decreasing by 5.15%.

- Loans growing by an eye-popping 6.75%.

I have worked in the financial services industry for over 30 years, and while these changes were shocking to me, I can understand both the decrease in deposits (pandemic relief drying up) and the shift in investment portfolios. Investments have matured, rate direction is unclear, and banks are sitting on large, unrealized losses. The combination of unclear rate direction and large unrealized losses makes banks hesitant to buy bonds.

The loan growth of 6.75% – almost double the annual loan growth rate from the five previous years (3.86%) – is surprising for two reasons.

First, with most economists forecasting a recession in 2023, I would expect financial institutions to be restricting credit at this point in the credit cycle. Second, in normal times based on the law of supply and demand – if we saw a dramatic rise in prices (i.e., significantly higher interest rates), we would expect to see a decrease in loan demand! (Remember college economics?)

These two facts make me wonder ... who is borrowing today and is their risk higher?

One thing I do know is “value shoppers” are not interested in borrowing given the high prices for products (due to inflation) and higher borrowing costs.

As a self-proclaimed value shopper, I bought two new cars shortly after the pandemic hit while inventory was high and both car prices and borrowing costs were low. I also refinanced my mortgage several years back to a 30-year mortgage at 2.875%. Personally, as a value shopper, I’m certainly not looking to borrow at today’s rates.

With value shoppers out of the market, there are some questions to consider:

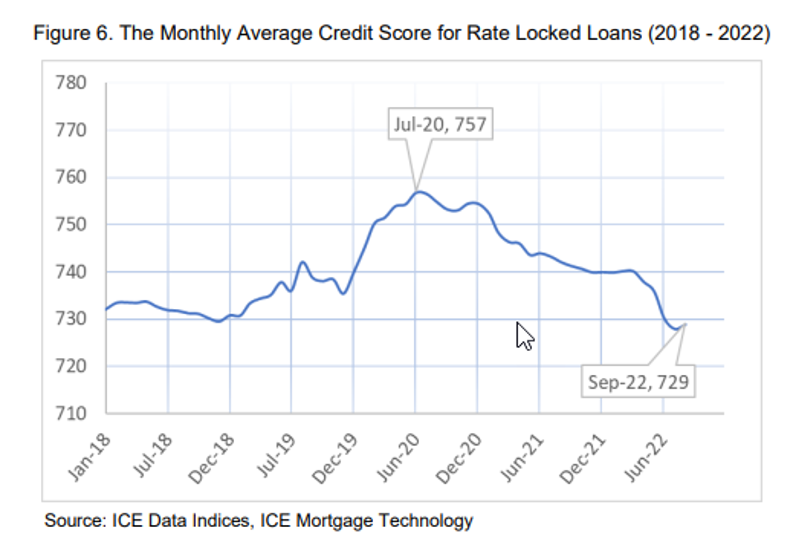

- What are the implications of the risk in your portfolio? (See monthly average credit score for rate-locked loans chart below.)

- Why are financial institutions increasing loan balances ahead of a likely recession?

- Are we reserving enough for the combination of economic slowdown and a potentially riskier portfolio?

To add some perspective, one of my colleagues opened a de novo bank in 2006 – two years before the Great Recession.

In 2009, he stated the previous year was hard, but he was glad they passed on several marginal deals in 2006 and 2007 – as they would have become defaulted loans during the Great Recession.

While my nature is to be optimistic and hopeful for a soft landing, we don’t know the future. Given the current economic climate, I encourage you to take a step back and remain cautious when granting credit.

For more content like this, subscribe to our blog – or visit the Financial Operations page on our website to learn more.

Happy New Year!

.svg)