A beloved coworker, long-time Jack Henry blogger, and veteran lender once shared a story that I’ll never forget. Many years ago, he met with a business owner to discuss his cash flow challenges and was considering a revolving line of credit. When asked what he would do with the extra cash, the business owner said, “I would use it to catch up on trade payables and increase my cash position, but the first thing I would do is buy myself two brand-new pairs of shoes.”

When asked why, he said, “Outside the window there, you see my mailbox. That mailbox is about the most important thing to me here at the office. You see, you probably get paid regularly – every two weeks. I get paid by my customers when they see fit to cut me a check. Some customers pay very well, but others … not so much. In rare cases, some never pay me. All I can tell you is that I run out to that mailbox 10 times a day looking for my paycheck, and I’ve burned out at least two pairs of shoes in the process!”

Similar stories play out thousands of times every week across the country. Small business owners are working to manage cash cycles and are often fighting for payments from their larger customers. The State of Small Business Cash Flow study by Intuit identified day-to-day cash flow issues as a major stress point. Here are a few meaningful findings:

- 69% of small business owners experienced sleepless nights due to concerns about cash flow.

- On average, U.S. small business owners have lost $43,394 by foregoing projects or sales, specifically because of insufficient cash flow.

- Among those with cash flow issues, nearly a third (32%) of small business owners could not pay vendors, loans, themselves, or employees.

Unfortunately, cash flow issues are nothing new. Every day, business owners must make decisions that affect their operating cash cycle: decisions about payment terms, inventory levels, and employee compensation. Daily life can be a balancing act. Cash flow is a matter of timing. Small business payments dictate cash flow, which determines creditworthiness, which affects opportunities for lending and financing short-term working capital needs. It’s a vicious cycle, and poor personal credit history is the number one reason for business loan denial.

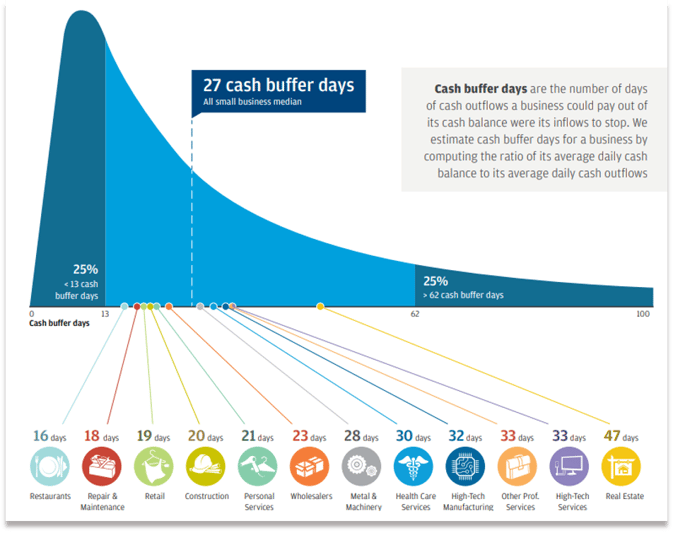

Cash Buffer Days

In the real world, payments are unpredictable. In the real world, large institutional customers tell the business owner they’ve changed their payments to 90 or 120 days, and they can “take it or leave it.”

The JPMorgan Chase Institute studied 600,000 businesses across a dozen sectors regarding cash flow issues for small businesses. The study shed light on how many days of cash businesses tended to maintain, a term they coined “cash buffer days.” Their findings revealed that on average, small businesses in the U.S. maintained a 27-day supply of cash on hand to meet short-term obligations. The study went on to explore specific industries and estimated averages for each.

Consider these two examples of businesses that rely on cash flow for survival:

- A staffing company’s accounts receivable makes up more than 45% of total assets on average – a substantial ratio. They’re challenged to meet weekly or bi-weekly payroll expenditures, despite their customers often paying them on Net 30 terms.

- A small trucking company’s accounts receivable average 32% of its total assets. They rely heavily on receivables to supplement weekly cash demand for payroll, hefty fuel costs, and short-term expenses.

The Importance of Regulating Cash Flows

Developing and executing a working capital strategy positions companies to seize growth opportunities, purchase inventory, take advantage of supplier discounts, increase staffing, and fund payroll. In fact, a lack of adequate working capital is the number one reason for business failures in the U.S. The JPMorgan Chase Institute cash flow study also revealed, firms with regular cash flows were twice as likely to survive as those with irregular cash flows.

Fintechs are Answering the Call

“Only 39% of businesses think their bank understands them. 90% wish they did.” - Barlow Research

Businesses are relying heavily on nonbank providers – not just to process incoming and outgoing payments, but also for an expanding array of banking and lending services. Small-business banking relationships are under siege from big-tech offerings such as Square Banking, QuickBooks Cash, and Shopify Balance to fintech innovators like Kabbage, BlueVine, and Brex. These providers are integrated with other essential business services to create alternative platforms that enable businesses to manage their finances outside the virtual walls of a bank or credit union.

Counter with Fundamental Competitive Advantages

Delivering personalized service, community expertise, industry specialization, and tailored product design can all still make a difference today. By providing secure payment solutions, innovative financial management tools, and access to more predictable working capital, banks and credit unions can help businesses optimize their finances and operations and grow. The latest Javelin report, 6 Keys to Building the Future of Business Banking, offers these tips:

- Make cash flow visualization and projection the focal point of the online banking experience. Provide business owners with a quick snapshot of their currently planned credits, deposit holds, debits, and resulting cash balance. Better still, go a step further and offer the ability to adjust projections and forecast cash position for days and weeks.

- Build products around cash flow tools. Enabling business accountholders to better understand their operating cash cycles is an opportunity for financial institutions to position timely and useful offers that help solve cash flow challenges.

- Help businesses get paid – quickly and reliably. The ability to create a payment request with a few details, send that request to the customer, and receive a low-cost, real-time payment is a large part of the proposition for most business owners. Enable businesses to include basic customer details and contact information, add products and services to the invoice, provide noncard payment options through a link or a QR code, and preview the invoice before sending it. Especially for those businesses currently creating paper or PDF invoices, these capabilities can save a lot of time and headaches.

- Provide customers and members with access, control, monitoring, and insight into their accounts receivable. Offer invoice scheduling, allowing accountholders to automatically send payment requests on a recurring basis to regular customers without creating a new invoice each time. Provide a library that enables businesses to view previous invoices and send reminders to pay outstanding invoices. Ultimately, aim to provide insights into accounts-receivable data and trends, enabling business owners to anticipate cash flow shortages. Use technology to provide them with instant cash flow in exchange for their accounts receivable.

Community and regional financial institutions can help businesses in their communities thrive (and save a lot of shoes) by removing the #1 obstacle to their financial health – insufficient cash flow.

-1.png?width=600&height=600&name=Retail-and-Small-Business-Banking-Img%20(1)-1.png)

.svg)